Nearly £8 million taken out in short-term loans in Calderdale over the last three years, figures reveal

and live on Freeview channel 276

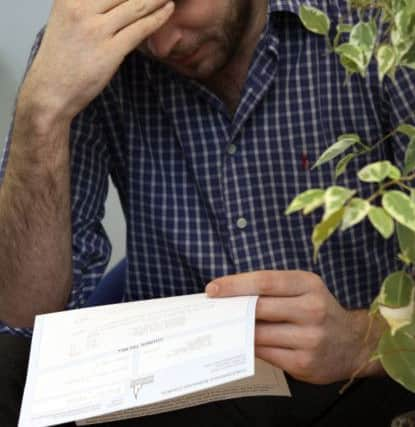

Figures released under the Freedom of Information Act reveal that 34,329 high-cost, short-term credit (HCSTC) agreements have been entered into in Calderdale since 2016, totalling £7,791,869.

The annual amount of agreements rose from 9,663 in 2016 to 11,542 last year, with the total amount borrowed rising from £2,100,788 in 2016 to £2,712,939 last year.

Advertisement

Hide AdAdvertisement

Hide AdThe Financial Conduct Authority’s definition of HCSTC agreements includes unsecured consumer loans with annual percentage rates of 100 per cent or more where the credit is due to repaid or substantially repaid within 12 months.

Figures obtained by the Courier also show that personal insolvencies through Debt Relief Orders (DRO’s), sometimes referred to a ‘mini bankruptcies’, have risen from 102 in 2016 to 243 in 2018.

Noah’s Ark Money Advice Service (NAMAS) is a specialist debt advice service based in Ovenden.

The service works predominantly, but not exclusively, with clients suffering from poor mental health.

Advertisement

Hide AdAdvertisement

Hide Ad“We see clients at each end of the spectrum,” says Andrew Sykes, “from those whose debts are making them suicidal to those suffering anxiety because they dread the post coming or the phone ringing.”

In 2016 and 2017, Noah’s Ark arranged around 60 per cent of the DRO’s completed in Calderdale: more than any other advice provider. “The upward trend in to 2018-19 is quite shocking,” said Andrew. “We did three times the number of DRO’s in 2018 compared to two years earlier. From the start of October 2018 to the end of March 2019 the figure was 140, around 23 per month, compared to five per month in 2016.

“Is there a link to high-cost short-term credit agreements? I would say yes but also there is a definite link to the wider introduction of Universal Credit across Calderdale in 2017.

“The Department for Work and Pensions (DWP) through Universal Credit is fast becoming the UK’s biggest debt collection agency.

Advertisement

Hide AdAdvertisement

Hide Ad“Rules allow the DWP to deduct up to 40 per cent directly from someone’s Universal Credit to pay for debts.

“We see clients week in, week out who are losing huge chunks of their entitlement because of third party debt deductions.

“And these debts can be for a multitude of different creditors: Universal Credit advance payments, tax credit over-payments, Council Tax arrears, benefit over-payments, gas, electric, water or rent arrears.

“We shouldn’t be surprised then that more and more people are being forced to turn to high cost short term lending when very often they don’t have enough money to feed themselves and their children.”

Advertisement

Hide AdAdvertisement

Hide AdAndrew believes the problem is getting worse and thinks organisations like Noah’s Ark are only touching the surface of the problem.

“If you look at our activity, which I have to say I’m really proud of given how much we do with so little income, referrals come to us by word of mouth, that’s to say we do nothing to proactively promote our service.

“Plus over 80 per cent of our clients come from North Halifax but the same issues exist in Todmorden, Brighouse and Elland etc.

“Our experience is that applying for a payday loan is symptomatic of a bigger problem. Everyone we’ve seen with a short-term loan has other debts and invariably needs debt advice not more lending.

Advertisement

Hide AdAdvertisement

Hide Ad“They would find that seeking professional help from a quality advice provider like Noah’s Ark would not only do them more good in the longer term but probably in the short term as well.

“The majority of our clients need a face-to-face advice service that will support them but they also need a quick outcome.

“As each month goes by their situation will only be getting worse. We have developed our service to be really fast.”

When asked what Andrew would like to see change to tackle the issue, he said: “Our local authority funding is now one third of what it was in 2016 but we have three times the workload.

Advertisement

Hide AdAdvertisement

Hide Ad“Calderdale residents need advice services like ours plus we contribute far more to the local economy than we take out.

“For example, in 2018 we took 433 complex debt referrals and completed 185 personal insolvencies. This wrote off £2,500,000 of problem debt.

“We also reinstated £156,000 of benefit income being lost to debt deductions and we received for clients over £28,000 of cash grants from grant making charities.

“All of this is money that our clients were free to spend in the local economy.

Advertisement

Hide AdAdvertisement

Hide Ad“We did all the above with just over £8,000 per annum from Calderdale Council. Will we have that funding in 2020? I have no idea.”

One Halifax mum spoke to the Courier anonymously about her experience of living with debt.

“When I was younger, maybe 18 or 19, I started getting into debt with things like mobile phones and council tax,” she said. “I was rubbish with money.

“I was at breaking point, and then I heard about Noah’s Ark through a friend. I spoke to Andrew and he understood the stress I was under.

Advertisement

Hide AdAdvertisement

Hide Ad“I didn’t want to answer my door because people were coming for money. I lived a very sheltered life because I was scared about opening my door due to the worry about people wanting money from me.

“It all just added to my stress. You can’t see a way out of it.

“I couldn’t pay for my daughter’s school uniforms or provide for her myself, which wasn’t a nice feeling

“But luckily I’ve got a good family around me so I had help from them.

Advertisement

Hide AdAdvertisement

Hide Ad“Then Noah’s Ark told me about Debt Relief Orders. I didn’t know anything about them.”

The woman also cited Universal Credit as a common reason why people get into debt.

“The amount of money they took off me each month - I was paying nearly £200 a month in debt and I was on the lower rate to start with,” she said.

“I don’t think they should be able to take so much money off people like that. They can take up to 40 per cent which leaves you with barely anything left.

“It causes a lot of problems with debt nowadays.

Advertisement

Hide AdAdvertisement

Hide Ad“They didn’t pay me for 11 weeks to start with, but thankfully my family were able to help me out because my wage alone wasn’t really enough to live off.

“I also had to take four weeks off work due to the stress of it all and to get my head together.

“I was getting behind with my rent, but my local MP sent a letter on my behalf and three days later I had all my money back paid.”

When asked what advice she had for people in debt, the woman said: “I think a lot of people are embarrassed by debt, like I was, so they don’t want to do anything about it.

Advertisement

Hide AdAdvertisement

Hide Ad“That’s why it went on so long for me. But there’s no need to be embarrassed because there are people out there in the same position, and there are people who can help.

“The relief you feel after you’ve got everything sorted, you feel so much better.”

Caroline Jones, chief executive of Citizens Advice Calderdale, said: “Our experience is that the number of clients accessing “pay day” loans is reducing and this will be as a result of the regulations imposed by the Financial Conduct Authority.

“However we do encounter clients who are reliant on expensive overdraft arrangements and in some cases high interest credit cards.

Advertisement

Hide AdAdvertisement

Hide Ad“This is an area being monitored by the Financial Conduct Authority yet no action has been taken to reform this activity.

“Although expensive high cost credit has become increasingly difficult to obtain, hardship only seems to be getting worse.

“Clients who are unable to obtain credit, or rely on friends and family, are increasingly presenting with priority arrears and/or cutting back on essential costs like food and home energy.

“Where people are encountering such hardship, I would urge them to seek advice and support as soon as they can.

Advertisement

Hide AdAdvertisement

Hide Ad“We will help people to maximise available income, manage problem debt and gain access to other schemes and services.

“Citizens Advice Calderdale can be contacted by telephoning 0300 330 9048 between 9.30 am and 1pm Monday to Friday, by visiting Customer First (Horton Street) between 10am and 1pm or by e mail via the website www.calderdalecab.org.uk.”

Simone Armitage, of the Calderdale Credit Union, said: “It is really shocking to see these numbers of requests for high cost credit in our borough. Calderdale is a relatively small area with a high percentage of retired residents and so this could possibly indicate that the majority of applicants are younger people who are struggling to make ends meet.

“I would advise strongly that they look at what the credit union could offer, and that could make a difference to what was left in the pay packet even when paying back a loan. Credit union loans are tailored to be affordable to suit the circumstances of the member. Also the credit union would encourage the member to save at the same time as borrowing thus building up a sum of money towards the future.

Advertisement

Hide AdAdvertisement

Hide Ad“In this way the loan is reducing as the savings are increasing plus if a dividend is paid, the member will receive that into their savings account. This is a prudent way of managing your finances. The credit union is a not for profit organisation serving the local community; it is owned and run by its members, the members are the shareholders.

“I am pleased to announce that the credit union has just been awarded the Fair Banking five stars Mark, for its loan product. It should be noted the Fair Banking means “your financial wellbeing”. This is the highest award that is given to financial organisations and the process involves and external body looking at how our loan product benefits the customer and if the product is fair and flexible.

“It’s also largely based on member/customer feedback, and our members rated our services very highly, which is the best testimony that a business like ours can get, their views on our services were truly heartening, not just for myself as the general manager, but the staff who deal with our membership every day. It should be noted that one of the unique things about a loan with a credit union, is the interest is always applied to a reducing balance.

“I would always urge any existing or potential new members who may be experiencing financial difficulties, to please talk to us first and we will help and support and when appropriate we always signpost people to other agencies, for

example we work closely with the CAB regarding debt advice.

Advertisement

Hide AdAdvertisement

Hide Ad“We also a have bill paying service, which we call our budget accounts, whereby the credit union will manage the payments that need to be made for our members, from rent/mortgage payments, any creditors that need to be paid, fuel bills etc., some of our members find this extremely beneficial especially as they navigate the changes of universal credit. Come and talk to us at our offices at 15-19 Commercial Street, Halifax. Or alternatively ring us on 01422386060 or visit our website www.calderdalecreditunion.co.uk.”

Sue Anderson, Head of Media at StepChange Debt Charity said: “Yorkshire and the Humber is the region with the third biggest proportion of StepChange clients, with 10 per cent of our clients based in the area.

“We are frequently witness to the problems short term high cost credit, such as payday loans or sub-prime credit cards, can cause. Almost one in five StepChange clients have short term, high cost credit agreements, with an average debt of £1,755.

“We would urge people to think carefully before taking out a short term high cost credit product, and consider whether they may benefit from free, impartial debt advice instead.”

Advertisement

Hide AdAdvertisement

Hide AdCoun Susan Press, Calderdale Council’s Cabinet Member for Public Services and Communities, said: “We are aware that people are struggling with money due to the impact of welfare reforms and we do everything we can to provide support, to help them manage their money and avoid debt.

“These figures relate to private loan agreements and although the Council has no control over these, we will use the data to help us understand if there are any emerging issues or particular trends.

“We work hard to support residents who are struggling to pay their Council Tax and housing costs, with our Council Tax Reduction Scheme and Discretionary Housing Payments. We also fund a number of organisations who provide debt and financial resilience advice to local people – our main advice contract is with Citizens Advice Calderdale but we also fund a number of other organisations to provide targeted advice for particular communities, in line with our Advice Strategy for Calderdale. Our Customer First Team helps many people to maximise their benefits.

“As part of our Anti Poverty action plan, Cabinet approved additional funding for three years to continue emergency welfare payments for those most vulnerable residents, after Government funding ended. Although this money is no longer available to local councils, we have not reduced the core budget for this work. However, this is being stretched further due to significant budget pressures and increased demand for services which we and community organisations are experiencing.”